- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 19, 2025 at 12:51 pm

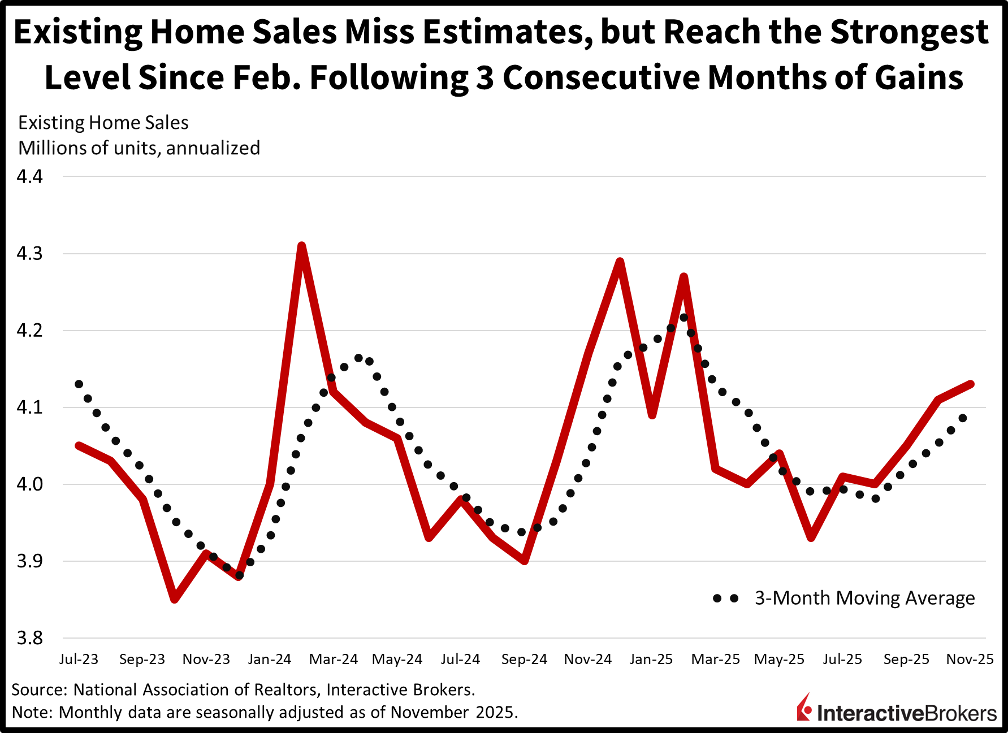

The post CPI rally is gaining steam as investors look to finish off the last final trading week of 2025 in stride by piling into tech stocks, cryptos and metals. Equities are getting closer to fresh records ahead of what’s historically one of the best periods on the calendar for share prices, but Treasuries are paring some of yesterday’s gains, as complications resulting from the longest government shutdown in history led to what was almost certainly an understated CPI. Indeed, the BLS relied on a carry-forward technique, due to the statistical collection lapse amidst limited days to publish the numbers, serving to totally suppress housing costs. Of course, there’s a small chance that the pivotal segment, which comprises the top weighting in the indicator at north of 41%, was nearly flat for October and November, however, there’s a much greater likelihood that the closely watched gauge will inflect higher by a tenth or so in December and January against the backdrop of the restoration of traditional methodologies and practices. To be clear, I do agree that the process of disinflation is underway and that cost forces are softening, yet I’m at odds with the 2.7% print and am more comfortable assuming a 2.8% figure at the moment. Meanwhile, today’s economic data wasn’t too friendly to bond bulls, as UMich’s 12-month inflation expectation was revised to 4.2% from 4.1%, contributing to the downgrade in overall shopper moods. The increase in yields was curbed by that miss on consumer sentiment as well as the separate existing home sales publication, with transactions continuing to be hampered by lofty mortgage rates and pricey valuations that together sustain subdued affordability conditions. Still, closings have improved for the third consecutive month and are at their strongest level since February. Outside of fixed income though, most things are catching bids, including 8 of the 11 major equity sectors, cryptocurrencies, forecast contracts and the greenback. The commodity complex is also advancing and features an all-time high for silver while gold is less than a percent from eclipsing its historic peak. Risk-on postures and lightening interest for hedges as a result are sending premiums on volatility protection instruments south.

A modest drop in mortgage rates alongside narrowing spreads relative to the Treasury complex helped bring buyers off the sidelines and drove an increase in existing home sales. The November result of 4.13 million seasonally adjusted annualized units missed the expectation of 4.2 million but improved from October’s 4.11 million amidst strengthening trends. The pace of closings ascended 0.5% month over month (m/m) while descending 1% year over year (y/y), as prospective purchasers and sellers continue grappling with valuations, concessions and decreasing inventories. Indeed, residential supply is lower by 5.9% m/m , however, it’s higher by 7.5% y/y, while median prices have only appreciated 1.2% y/y. The anticipation that wage gains are going to keep exceeding growth in real estate values is encouraging for an industry that has struggled to regain its mojo for almost 4 full years now. Meanwhile, key exchanges were led by the single-family segment which rose 0.8% m/m while condos/coops saw a 2.6% decline. From a regional perspective, the Northeast and South experienced m/m increases of 4.1% and 1.1%, the West was flat and the Midwest was down 2%.

Against the backdrop of a light economic calendar to end 2025 amidst the most significant and timely reports already dealt with, there’s little standing in the way for stocks to stage a Santa Claus rally. Favorable seasonals, subdued volumes, limited publications and a jolly mood on Wall Street are to be expected, which are conducive to greater risk appetites in the final sessions of the year. But rates will be trickier, as fixed income watchers will certainly be paying attention to the scheduled prints which include 3rd quarter gross domestic product, ADP’s weekly employment gauge, unemployment claims, durable goods, industrial production, and consumer confidence. None of these releases are likely to influence trading action much, since they’re either stale due to the shutdown, noisy and high-frequency, or generally lower-profile relative to the heightened importance of the Consumer Price Index or nonfarm payrolls for example.

The Bank of Japan (BoJ) hiked its benchmark rate by 25 basis points (bps) and communicated that more increases are on the way in light of robust wage growth and elevated inflation. The nation’s currency weakened following the news, however, as stretched positioning was likely looking for an increasingly hawkish message to extend gains.

Conversely, the Bank of Mexico (Banxico) cut its rate by 25 bps despite accelerating inflation as the divided board is increasingly worried about weak economic growth amidst the adverse impact of Washington’s tariffs.

Japan’s Consumer Price Index (CPI) held pretty steady last month with headline increases of 0.4% m/m and 2.9% y/y, the same pace as October on the monthly and a tenth lighter on the annualized. The y/y core number, which excludes food and energy due to their volatile characteristics, stayed unchanged at 3%, which was in-line with estimates.

Euro zone consumer confidence slipped to -14.6 this month from -14.2 in November and missed the expectation for an increase to -14.

UK Consumer confidence rose from -19 to -17, exceeding the expected -18 and helped by an increase in plans to make major purchases in the near future. High taxes, heavy job losses and elevated interest rates continue to stress households, however.

This morning’s retail sales reports from Canada and the UK served bifurcated November results. The former nation saw a 1.2% m/m increase, which marked a recovery from the 0.2% decline in October. Conversely, the latter experienced a drop of 0.1% m/m, despite expectations calling for a 0.4% climb. The contraction was shallower than the 0.9% decrease in the prior month, however.

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Futures, event contracts and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy visit our Warnings and Disclosures Page.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!